Kickstart Your New Year with Financial Wellness Month: Tips, Stats, and a Fresh Start

The New Year always feels like a breath of fresh air—it’s a chance to pause, reflect, and plan for the next 365 days. For many of us, January becomes the perfect time to reevaluate our money habits, set meaningful goals, and create a roadmap to better financial health. It’s no coincidence that January is also Financial Wellness Month, highlighting the importance of taking care of our financial well-being just like we do our physical and mental health. If you’ve been wanting to start your year on a more stable financial note, read on. We’ll talk about why Financial Wellness Month matters, share some interesting statistics, offer practical tips to make this your best financial year yet, and show you how a financial advisor can help guide you along the way!

Why Financial Wellness Matters

Financial wellness is more than just having an emergency fund (though that’s certainly a good start!). It’s about your overall relationship with money—managing debt, building savings, planning for retirement, and even thinking about how finances affect your emotional and mental well-being. According to a recent survey, around 60% of Americans live paycheck to paycheck, which can contribute to stress, anxiety, and a constant feeling of being on edge. By setting financial goals early in the year, you can reduce that stress and empower yourself to feel more secure and confident in your day-to-day life.

Set the Tone for the Entire Year

1. Start with a Financial Checkup

Just like you’d get an annual physical or tune up your car, it helps to do a yearly review of your finances. Write down all your incoming money (salary, freelance gigs, side hustles) and outgoing expenses (bills, loans, rent, credit card payments). Often, seeing these numbers clearly laid out is the wake-up call we need to move forward with intention.

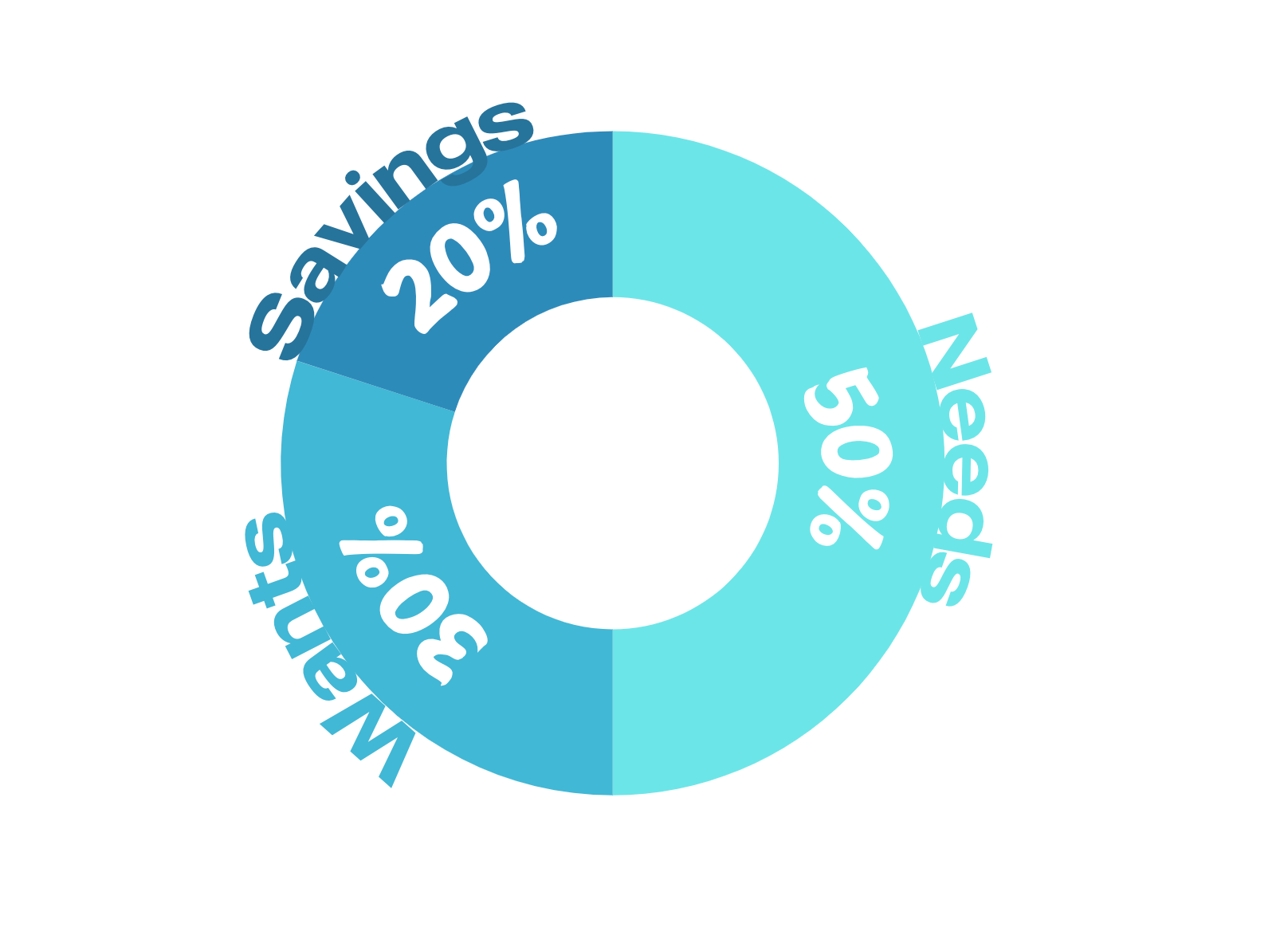

2. Create (or Update) Your Budget

Budgeting can sometimes feel restrictive, but think of it as your personal road map instead. A popular and straightforward method is the 50/30/20 rule:

- 50% of your income goes to needs (housing, utilities, groceries).

- 30% goes to wants (dining out, entertainment, hobbies).

- 20% goes to savings and debt repayment (emergency fund, credit card debt, student loans).

Adjust the percentages to fit your lifestyle, but aim to include a dedicated line for savings and debt repayment. Treat these categories as “must-pays,” just like your phone bill, so you never skip out on building a stronger financial safety net.

3. Build or Boost Your Emergency Fund

Having an emergency fund is one of the best ways to protect yourself against life’s unexpected twists—car repairs, medical bills, or sudden job loss. Experts often recommend saving three to six months’ worth of expenses in an emergency fund. If that feels overwhelming, start with smaller steps. Even setting aside $20 a week can make a difference over time.

4. Reduce (and Tackle) Debt

January is a great time to tackle any lingering debt—from credit cards to student loans—head-on. Consider consolidating high-interest credit card debt into a lower-interest loan, or create a repayment strategy that targets the highest-interest debts first (the “avalanche method”). If that method feels too daunting, try the “snowball method,” where you start by paying off the smallest debt first, building motivation as you knock out one balance at a time.

5. Set Clear, Specific Goals

Vague resolutions like “I want to save more” can be less motivating than specific goals like “I want to save $5,000 by December” or “I want to pay off $2,000 in credit card debt by June.” Write these down, break them into monthly or weekly targets, and track your progress. Watching those numbers inch closer to your target can be super rewarding!

Where and How a Financial Advisor Can Help

Sometimes, tackling all these financial tasks can feel overwhelming—especially if you’re juggling work, family, and other responsibilities. A financial advisor can offer expert guidance, keeping you on track and tailoring strategies to your unique situation. Here’s how they can help:

- Personalized Financial Planning: Advisors can build a custom plan based on your income, expenses, debt, and long-term goals. They’ll help you prioritize which debts to tackle first and how much you should allocate toward savings and investments.

- Investment and Retirement Guidance: Unsure of where to put your money for long-term growth? An advisor can help you create a diversified investment portfolio and ensure you’re making the most of retirement accounts like a 401(k) or IRA.

- Accountability and Ongoing Support: It’s easy to lose motivation if you’re going it alone. With regular check-ins, a financial advisor can celebrate your progress with you and help you recalibrate if something isn’t working.

- Risk Management: Life happens, and an advisor can guide you on the right types of insurance and protection to safeguard your finances.

- Estate and Legacy Planning: If you want to plan for future generations or ensure your affairs are in order, an advisor can walk you through wills, trusts, and beneficiary details.

Tracking Your Progress and Staying Motivated

It’s easy to set goals in January but lose steam by spring. Keep the momentum going with a few motivating strategies:

- Automate Your Savings: Schedule automatic transfers to your savings account right after your paycheck hits.

- Use Apps for Accountability: Budgeting tools like Mint, YNAB (“You Need A Budget”), or a simple spreadsheet can help keep track of income, expenses, and savings.

- Celebrate Milestones: Paid off a credit card? Saved your first $1,000? Treat yourself with something small or plan a fun, low-cost activity. Celebrating progress can help you stay excited and committed.

Final Thoughts

Financial Wellness Month is a reminder that our financial health deserves just as much attention as our physical and mental well-being. Whether you’re a budgeting newbie or someone looking to refine your money management skills, there’s no better time than right now to set clear goals and create habits that will serve you for the rest of the year—and beyond.

Remember, small steps add up to big changes, so don’t be discouraged if you’re starting small. By celebrating little wins, staying the course, and seeking help from a financial advisor if needed, you’ll be amazed at how much progress you can make by next Financial Wellness Month. Here’s to a financially sound and stress-free year ahead!