How Much Holiday Cheer Is Too Much? A Look at Americans’ Growing Seasonal Debt

The holiday season is a time for celebration, giving, and—unfortunately for many—taking on extra debt. According to a recent LendingTree survey, Americans who used credit or other payment methods to finance their festivities this past year ended up with an average of $1,549 in new holiday debt, a jump of 24% from the previous year. While everyone loves the magic of the season, no one loves dealing with its lingering financial aftermath.

In this blog post, we’ll explore the key findings from the survey, look at the reasons behind this spike in holiday debt, and consider practical tips for getting ahead of it before next year’s celebrations roll around.

1. The Rising Tide of Holiday Debt

A Bigger Bill Than Before

A significant 36% of holiday shoppers indicated they took on extra debt to pay for gifts, travel, and other seasonal expenses. Their average holiday debt hit $1,549—nearly a quarter more than the previous year. Various factors may explain why Americans are spending more, including soaring living costs, holiday travel expenses, and the pressure to keep up with gift-giving traditions.

Credit Cards Dominate, But BNPL Is Growing

Credit cards remain the go-to method for handling holiday purchases—most holiday debt was charged to plastic. However, buy-now-pay-later (BNPL) services are on the rise, with more than a fifth of surveyed shoppers saying they used BNPL for holiday spending. While flexible financing options can offer short-term relief, they can also lead to confusion or missed payments down the line if not managed carefully.

2. Who’s Feeling the Pinch?

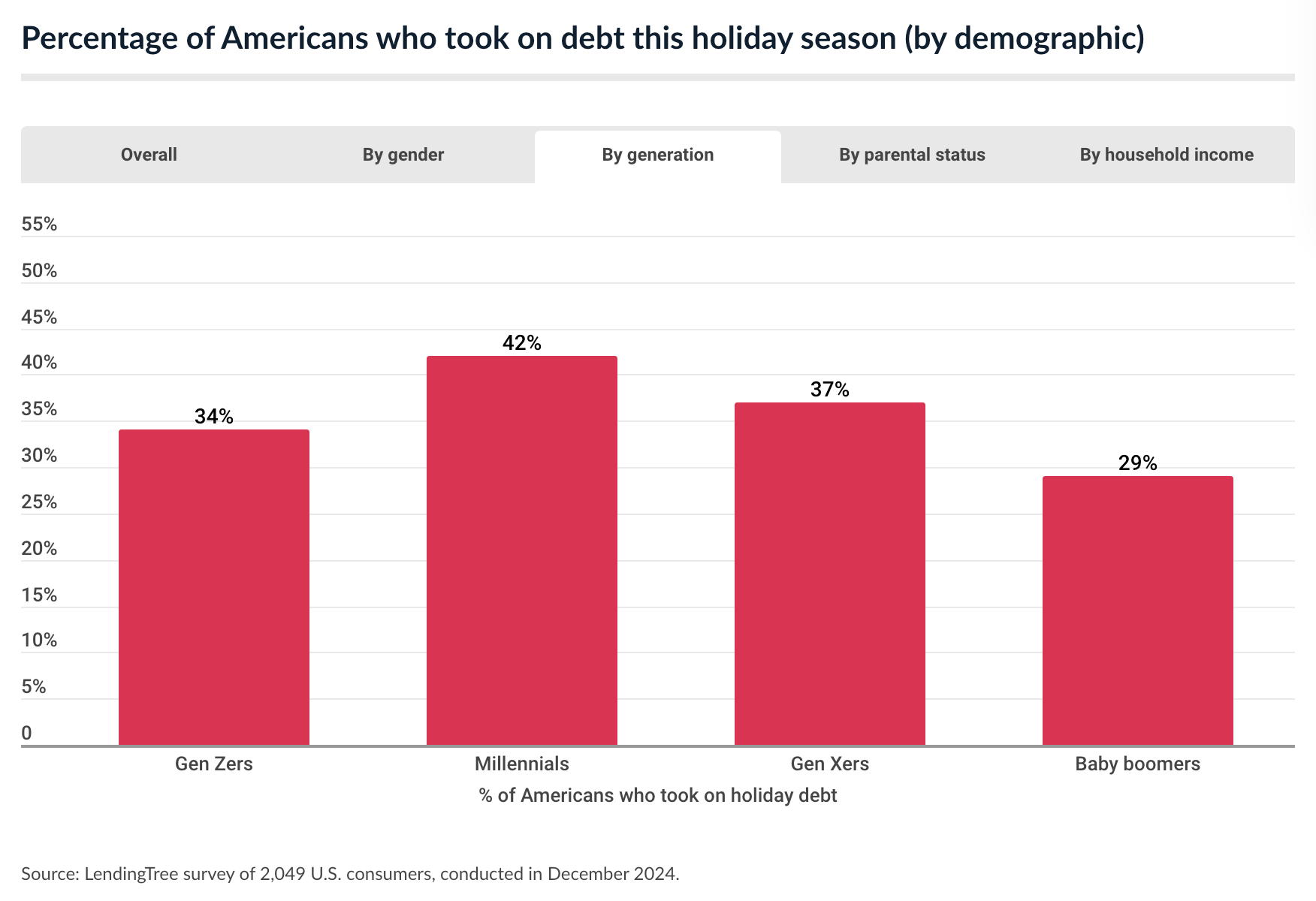

Debt by Generation

- Millennials: The highest percentage of users who reported taking on new debt, at 44%. This could be tied to ongoing financial responsibilities like raising children and buying homes.

- Gen Z: 37% took on holiday debt. While younger, many are still establishing credit histories and may be more susceptible to high interest rates or less favorable lending terms.

- Gen X: 36% admitted to taking on seasonal debt, facing pressures like supporting kids and aging parents simultaneously.

- Baby Boomers: 28% took on new debt, possibly reflecting fixed incomes or a desire to maintain long-standing family traditions.

Regret and Repayment Challenges

Not everyone feels confident they can pay off these debts quickly:

- A substantial portion of respondents admitted they’d need more than three months to fully clear their balances.

- About 12% reported no confidence at all in their ability to repay.

3. Why Holiday Debt Adds Up Quickly

Rising Costs

Inflation doesn’t take a vacation during the holidays. Higher grocery, travel, and entertainment costs can quickly blow up budgets.Gift-Giving Pressure

Many people stretch themselves too thin by buying gifts for extended family members, friends, and colleagues. This generosity, while well-intended, can leave budgets in the red.Impulse Spending

Festive moods often lead to impulse buys or last-minute splurges. Whether in-store or online, sales and promotions can tempt shoppers to overspend.Travel Expenses

Seeing loved ones is often a key part of the season, but flights, gas, and hotels can significantly inflate holiday bills.Buy-Now-Pay-Later

Although BNPL can make big purchases feel more manageable in the moment, these smaller installments still add up—often at higher-than-anticipated interest rates or fees if payments are missed.

4. Smart Strategies to Avoid a Festive Financial Hangover

Set a Realistic Holiday Budget

Determine what you can comfortably spend without dipping into savings or maxing out your credit cards. Consider allocating funds for gifts, travel, and festivities separately so you don’t lose track of how much you’re shelling out overall.Shop Early—and Mindfully

Spread out your holiday shopping through the year. By taking advantage of off-season sales and discounts, you’ll avoid that frantic (and often expensive) last-minute gift rush.Explore Low-Interest or No-Interest Options

If you need to finance holiday spending, consider a 0% APR introductory credit card or a lower-interest personal loan rather than relying solely on high-interest credit cards. Just be sure to pay down the balance before the promotional period ends.Use BNPL with Caution

Buy-now-pay-later services can be helpful if you stick to a repayment plan—but keep track of all your installments to avoid overextending your budget.Simplify Gift-Giving

Homemade gifts, gift exchanges with a spending cap, or experiences rather than material goods can all help keep costs under control. Often, a thoughtful gesture means more than a high price tag.Plan for Next Year

Once the decorations come down, take stock of this year’s spending. Could you start saving a little each month for the next holiday season? Even setting aside a modest sum can prevent a debt pileup down the road.

Conclusion

With the average American holiday debt surpassing $1,500, it’s clear that seasonal spending can leave a lasting impact on personal finances. Yet the pressure to celebrate in style doesn’t have to mean breaking the bank or living with lingering balances well into the new year.

By setting firm budgets, exploring lower-interest financing options, and resisting impulse spending, holiday shoppers can maintain the generous spirit of the season without seeing red on their credit card statements. Remember that the best gift you can give yourself is a stable financial future—long after the tinsel is packed away.

If you find yourself in a tricky spot post-holiday, don’t hesitate to seek professional advice on managing credit card balances or personal loans. With a little planning and discipline, you can ensure that next year’s festivities are every bit as bright—minus the dreaded debt hangover.

Disclaimer: The data and findings presented here come from LendingTree’s survey on holiday spending and debt. Always conduct your own research or consult a financial professional before making major financial decisions.