The current estate tax exemption amount is historically high, but it’s scheduled to “sunset,” on December 31, 2025, unless Congress acts. Most of you likely believe you don’t have enough assets to worry about federal estate taxes, but if this sunset occurs, you may be impacted– and if not immediately, at some point in your future.

Here's what we will discuss:

- What exactly the estate tax exemption is – and will be

- Which clients could be impacted

- How you can help clients prepare

- The estate tax exemption may be cut in half or more.

The Tax Cuts and Jobs Acts (TCJA) of 2017 increased the lifetime federal estate tax exemption amount from $5.6 million to $11.18 per individual, indexed for inflation. In 2024, the exemption amount is $13.61 million per individual and $27.22 million per married couple. This means individuals can transfer up to these amounts to their heirs, either during their lifetime or at death, without paying any federal gift or estate tax. Any assets above this exemption would be subject to a 40% transfer tax.

With this act, most Americans no longer had to think too much about estate transfer taxes. However, this exemption is scheduled to sunset on December 31, 2025, unless Congress acts to extend or make it permanent. If nothing is done, the exemption amount will revert to $5.6 million per individual – indexed for inflation. Most experts project this will likely be around $6 million per person and around $12 million per couple. As a result, a huge portion of Americans will have to start thinking about federal estate taxes again.

Also, don’t forget that the state of Minnesota also has an Estate Tax separate from the Federal Estate Tax. In Minnesota, each spouse gets an estate exemption of $3 million. This $3 million is not portable, meaning your spouse does not automatically inherit your $3 million dollar exemption if you predecease them. This makes properly structured estate plans of the utmost importance in the state of Minnesota.

- More families may be impacted than you might think.

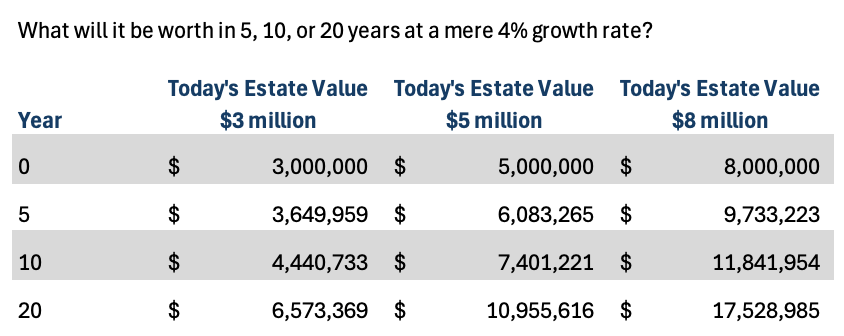

Even with these changes, many of you still won’t be impacted by federal estate taxes. And while that could be true, it could impact you more than you might think due to estate growth. According to the chart below, even individuals with an estate worth $3 million today might have to be concerned about federal estate taxes in the future due to growth over time.

Another issue is that a lot of families don’t consider insurance to be part of their taxable estate…but in some cases it is, which would immediately put a lot of people in this boat.

- There are ways clients can prepare to reduce their future tax burden now.

Many of you may be unaware of this potential coming sunset, and many of you may not believe it will ever apply to you or your family. You have a fantastic opportunity today to review your financial situation and estate documents and act. Here are a few steps to consider:

- Understand your taxable estate’s worth, including insurance, both as it stands today and as it grows.

- Estate Exemption uses gross values. This means that the deferred tax accumulated in your traditional IRA’s and 401(k)’s are included in your gross estate. Roth conversions can help reduce the gross value of your estate and have the potential to leave your heirs more assets after tax.

- Work with your advisor to develop a financial plan that gives you confidence that your retirement expenses can be covered so you can have a better picture of how much wealth you could pass to beneficiaries.

- If you can afford to do so, consider making lifetime gifts. The annual gift tax exclusion is $18,000 per beneficiary for 2024.

- Your heirs need the money now more than they need it when you are gone. If you are worried about your heirs squandering the funds, consider making contributions to their retirement accounts on their behalf. You may also consider funding a 529 education savings plan for children or grandchildren.

- If you currently have a taxable estate, consider how you can maximize the lifetime federal estate tax exemption amount today — especially if it decreases.

- The tax savings always need to be weighed against the costs and complexity. As Dave often says, “the Burden of Complexity” can outweigh the benefits.

If this is something that concerns you, feel free to reach out to our team. We would be more than happy to review your situation and point you in the right direction, should action be needed.